Morning Lineup – Here We Go Again!

Just when you thought the days of markets opening down sharply in reaction to an overnight headline concerning trade negotiations with China were over, we get this morning. There isn’t a whole lot of earnings data to contend with and the economic calendar is blank for today, so it looks like just three days after Kudlow decided to spike the ball in reaction to Friday’s NFP report, the President is shaking things up a bit with his tweet-storm last night.

US futures are set to open down over 1%, but the gains don’t look to be anywhere near as severe as what happened in China where the decline was more like 5%. Also, ever since the initial gap down, things have been extremely steady. Today’s decline is set to be the 9th gap down of 1% or more for the S&P 500 since the start of 2017, and in today’s Chart of the Day we looked at how the index performed following prior occurrences as well as what the catalyst for each decline was, so if you haven’t already seen it, check it out.

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

Last night’s sell-off in Chinese equities put a big dent into this year’s gains for the Shanghai Composite. With a drop of more than 5.5%, it was the largest one day decline for Chinese stocks since February 2016. Year to date, the Shanghai Composite is now up 16.54% on the year and has nearly cut this year’s gains in half. More noteworthy is the fact that with the S&P 500 up 17.5% YTD heading into today, the US is now outperforming Chinese stocks YTD. Obviously, with futures down over 1%, the US lead may not last for long, so we’ll have to see how things shake out over the course of the trading day.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Chart of the Day: 1%+ Gaps Lower at the Open

Bespoke Brunch Reads: 5/5/19

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2019 Annual Outlook special offer.

Investing

How Schwab Ate Wall Street by Lisa Beilfuss (WSJ)

Charles Schwab was once a simple discount broker, but while the company still competes on price as hard as it can, its more comprehensive model is now offering a more comprehensive suite of financial services to its growing client base. [Link; paywall]

Regional Stories

Can ‘Ma’am’ Be Saved? by Kathleen Purvis (The Bitter Southerner)

An ode to southern gentility, and a simple word often assumed to be snark by anyone not raised or immersed in a culture where genuine politeness is still appreciated. [Link]

California’s population growth is the slowest in recorded history by Javier Panzar and Sarah Parvini (LAT)

While more than 185,000 new Californians were minted in 2018, the rate of growth for the Bear Flag Republic is the slowest since at least 1900, presenting unique challenges for a state that’s never known anything but surging inflows of new residents. [Link]

Media Matters

A doorbell company owned by Amazon wants to start producing “crime news” and it’ll definitely end well by Joshua Benton (Nieman Lab)

Security technology company Ring (a subsidiary of Amazon) is looking to create some buzz by creating content based on crime reports in order to juice demand for Ring products. [Link]

The Lo-Fi Voices That Speak for America by Zack Stanton (Politico)

Once ubiquitous, AM radio is losing ground to FM and other new forms of digital audio, but the lower fidelity broadcast world is still a powerful medium that reaches millions of people every day. [Link]

Working Ways

Microsoft, Slack, Zoom, and the SaaS Opportunity by Ben Thompson (Stratechery)

Thompson walks us through the software-as-a-service world, focusing his lens on the largest (and least-associated) SaaS name out there: Microsoft. He also focuses on the strategic challenges the company now faces in a pure-SaaS world where new markets are being created. [Link]

‘996’ Is China’s Version of Hustle Culture. Tech Workers Are Sick of It. by Lin Qiqing and Raymond Zhong (NYT)

9am to 9pm, 6 days a week: that used to be table stakes to participate in China’s tech industry. But employees, feeling they aren’t getting the promised rewards of that trade-off, are pushing back. [Link; soft paywall]

Stripe’s fifth engineering hub is Remote by David Singleton (Stripe)

While the payments company still has engineering hubs in San Francisco, Seattle, Dublin, and Singapore, their newest location has no location, part of a growing trend of remote-first orientation for tech workers. [Link]

Demand Surges for Software ‘Robots’ That Automate Back-Office Tasks by Angus Loten (WSJ)

Menial labor in back-office tasks is increasingly being dumped on software companies that use software to replicate – with higher speed and accuracy – jobs that clerks used to do. [Link; paywall]

Real Estate

Unraveling Mark Zuckerberg’s Secret Deal for a $59 Million Tahoe Compound by Katherine Clarke (WSJ)

The billionaire Facebook founder has been snapping up huge, pricey properties across multiple states, burying the transactions under layers of LLCs and NDAs. [Link; paywall]

Theoretical Finance

A Legal Theory of Finance by Katharina Pistor (SSRN)

This paper argues that financial markets are not consistent with rule of law (especially enforcement of contracts) because those markets sometimes demand suspension of that law during times of extreme crisis. [Link]

Leftovers

First World War mustard gas leaks from Belgian underwater grave by James Crisp (Telegraph)

35,000 tons of munitions have been left underwater in the North Sea, but recently mustard gas leaked out near the Belgian Coast. [Link]

Music

Hymns drop off top 10 funeral music choices in favour of Ed Sheeran by Rebecca Smithers (The Guardian)

A UK funeral company has released a top ten list of most-requested funeral music. My Way by Frank Sinatra, Always Look On The Bright Side Of Life from Monty Python, and Ed Sheeran are some of the most popular tracks. [Link]

WTF

The Stolen Kids of Sarah Lawrence by Ezra Marcus and James D. Walsh (NY Mag)

The mind-bending story of a group of friends at Sarah Lawrence, the NYC-adjacent liberal arts college. Cult-like behavior driven by the father of one of the students gradually spiraled out of control with horrifying results. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Closer: End of Week Charts — 5/3/19

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. We also take a look at the trend in various developed market FX markets.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

The Bespoke Report – Cut it Out!

In the market’s ceaseless determination to make a mountain out of every molehill, equities sold off sharply from record highs on Wednesday afternoon after Fed Chair Powell suggested that the FOMC had no plans to cut interest rates as futures markets were implying. Didn’t he have some nerve?

In the last month, Jobless Claims hit a 50-year low, Q1 GDP surprised to the upside and came in at 3.2%, the stock market was at record highs, and on Friday, Non-Farm Payrolls surprised to the upside with a reading of 263K. Are there some blemishes on the landscape? Do things always look brightest at the peak? Sure, but to say the Fed must cut rates in this environment was a bit much. By the end of the week, cooler heads prevailed, and the S&P 500 finished the week less than 20 cents off its record closing high and less than ten points below its intraday record high.

Even more encouraging was the rally in the small-cap Russell 2000, which finally broke above resistance to close at its highest level since October. Traders often look to small caps for confirmation of a rally, and while we think they are often given more importance than they deserve, their outperformance this week doesn’t hurt.

We have a lot more to cover this week, including updates on some of the key leadership groups/indicators, drivers of the market’s strength in April, how earnings season is progressing so far, how the economy is faring, and the state of consumer sentiment, among other things. To read our full Bespoke Report newsletter and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

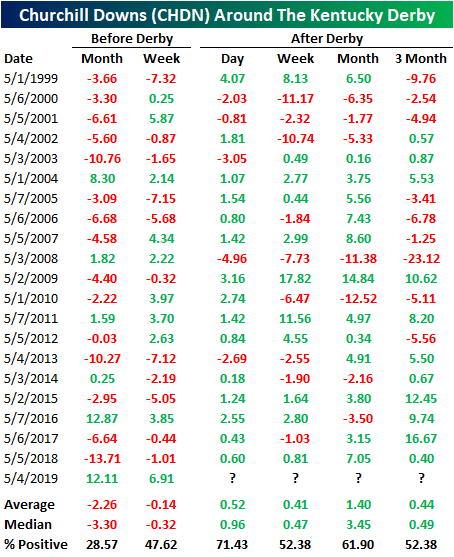

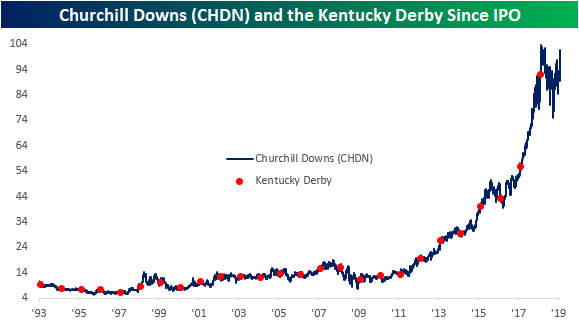

Churchill Downs (CHDN) Off To The Races?

The “Fastest Two Minutes in Sports” is on Saturday at Churchill Downs in Kentucky. Since the founding of the race and racetrack (in which the company draws its name) in 1875, Churchill Downs Incorporated (CHDN) has branched out to a number of other lines of business including ownership of other race tracks and casinos around the US in addition to online gambling sites. CHDN has been like Secretariat over the last decade, posting a “10-bagger” by rising more than 10x in value since its low in 2009.

So how does the stock perform around “Derby Day” specifically? In the past 20 years, the period leading up to the Kentucky Derby has typically been pretty shaky for the stock with declines in the month and week leading up to the race. Historically, in the month before the derby, CHDN has only risen 28.57% of the time with an average decline of 2.26%. The week before has been slightly better, but still declines over half the time. This year bucked the trend, though, with the stock rising 12.11% over the past month and 6.91% in the past week; similar to 2016.

Looking forward, returns have typically been positive in trading the Monday after the Kentucky Derby with a gain averaging 0.52%. Both one week and three months after, outperformance is similar rising 0.41% and 0.44%, respectively, on average. Both have also been positive only a little more than half the time. One month out has been a little stronger as CHDN has been more consistently positive, rising 61.9% of the time, and averaging a 1.4% gain.

Fortunately, recent history points to a bit more of an optimistic outlook. Many of the declines occurred in the 90’s and pre-crisis era. In the current bull run, the stock has only been lower one month out three times and only twice 3 months out. One final note, the company has typically reported their Q1 earnings around this time (sometimes even the trading day before or after the derby) . In other words, performance at this time of year is not purely a factor of the race as earnings also can have a significant impact. Start a two-week free trial to Bespoke Institutional to access our interactive Earnings Database, Seasonality Tools, and much more.

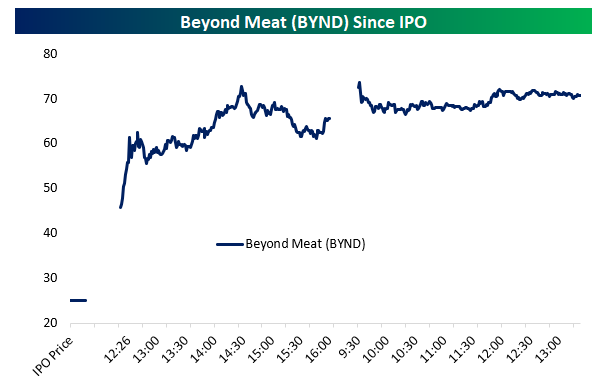

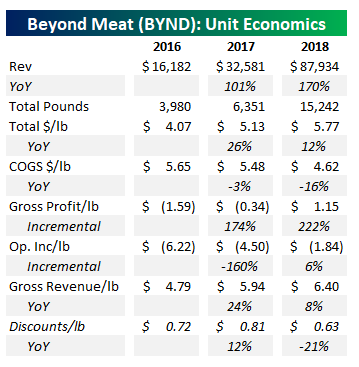

Beyond Meat (BYND) Brings Home The Bacon

Yesterday Beyond Meat (BYND) IPO’d at $25/share, valuing the business at about $1.5bn versus trailing 12-month revenues of less than $70mm. The company has been operating in VC-funded private markets for a long time, developing meat alternatives appealing to the health conscious, climate-concerned, and animal welfare-oriented consumer base that wants “meat” without some of its negative externalities. While the pricing of the IPO sounds aggressive, price action since has been extreme. The stock has surged more than 180% from its IPO price, trading in the low-$70 range and holding opening day gains as-of this writing.

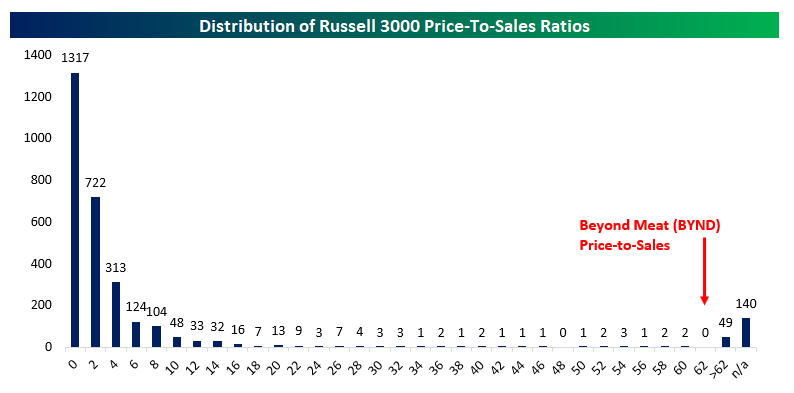

The nose-bleed 60.9x price-to-sales ratio BYND now carries sounds absolutely ridiculous, but there are actually 49 companies in the Russell 3000 with a more aggressive valuation and another 140 for which data is not available. Obviously, BYND’s valuation relative to its sales is extremely aggressive, but given its long history in the private markets, describing it as an extremely high-growth company isn’t without precedent among current listed stocks in the US.

While it’s hard to get excited about a stock that has so much optimism priced in already, we should note that BYND’s economics don’t actually look as bad as some other IPOs and businesses we have come across. This is a real business, with real demand, what appears to be pricing power, and potential to grow very profitably. In the table below, we show annual data from Beyond Meat’s S1. Revenue has more than doubled the last two years, with the volume of meat substitute products rising by almost 5x in two years. As the company has scaled up its product offering, it has raised prices from an average net of $4.07 per pound to more than $5.70 per pound. At the same time, it has reduced discounting from 81 cents per pound in 2017 to 63 cents per pound this year.

On top of raised prices, the company has been able to reduce the cost of goods sold per pound, falling from $5.65 in 2016 to $4.62 today (down 16% YoY). Those positive economies of scale suggest that strong revenue growth will feed through to increasing profit margins. So far, that’s what’s happened: for each pound sold in 2016, BYND lost $1.59 on a gross basis, but gross profits rose by $1.74 for each additional pound sold in 2017 and by $2.22 cents per pound from 2017 to 2018. That’s led to gross profits of $1.15 per pound in 2018, and operating losses of $1.84 per pound in 2018. While the company used to lose money on each additional pond ($1.60 from 2016 to 2017), incremental pounds sold generated 6 cents of operating income per pound from 2017 to 2018. Assuming the company can keep up sales momentum and reduce costs across that higher volume, profitability is very attainable.

One last point on the BYND IPO: it’s part of a boom in average gain on the first day of trading. In the chart below we show the rolling three month average gain from IPO price to first close since 1995. The tech bubble really stands out on this chart! The average IPO went from a ~20% pop in the late 1990s to more than doubling! After 2001, pops returned to a much more normal 10-20% range, with some brief drops into negative territory during 2008, 2010, and 2016. With the most recent round of IPOs, though, we’ve seen the return of high average pops, and the current rolling three month average has shot up to nearly 30%. That’s the highest since the tech bubble, and highest for any period other than the tech bubble since 1995. So far, we’ve been pretty skeptical of claims that we’re in the same sort of period of market excess as the tech bubble (see “Best and Worst Performing IPOs” from April 23rd, link). This is one indicator, though, that points to the current IPO market being a little too hot. Other indicators, as discussed in that prior post, aren’t sending the same signal…for now, at least. Start a two-week free trial to Bespoke Premium to access our interactive earnings database and much more.

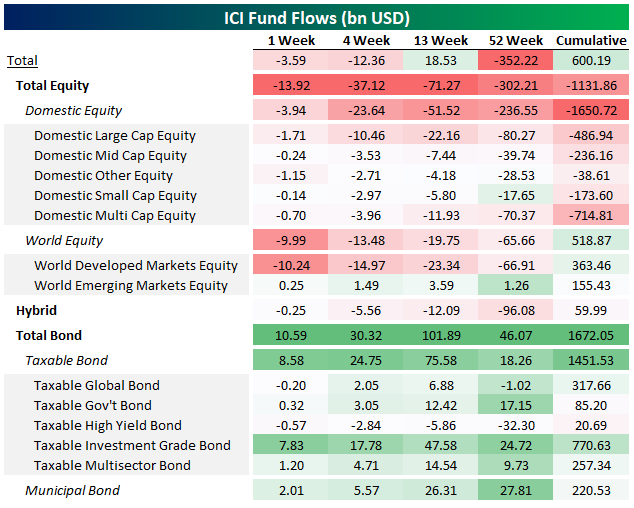

Mutual Fund Flows: A Tale of Two Asset Classes

Earlier this week the Investment Company Institute (ICI) reported mutual fund flows for the week ending April 24. The results were grim for the equity mutual fund industry, as they have been for a very long time. In the chart below we show dollar flows by mutual fund type across a variety of time periods. Notably, equity funds are extremely weak across almost all fund types, with emerging markets equity funds the only exception. The complete opposite is true of bond mutual funds. While equity funds saw outflows of $13.9bn over the course of the week, bond funds saw inflows of more than $10bn, driven by investment grade bonds. Start a two-week free trial to Bespoke Premium to access our interactive economic indicators monitor and much more.

Arbitrary large dollar numbers can be a bit hard to get a grasp of, so we also like to look at fund flows on a percentile basis, comparing their size to historical ranges. Higher numbers indicate larger fund inflows, or smaller outflows, while lower numbers indicate larger fund outflows or smaller fund inflows. This table ultimately tells the same story as the table above: very large outflows relative to history for equities, very large inflows relative to history for bonds. As with EM equities, there are exceptions to the bond inflow story: high yield has been relatively weak persistently of late. But generally speaking, fund inflows to bonds have been very large for a while now.

In the chart below we show cumulative fund flows for all US mutual funds, all equity mutual funds, and all bond funds. As shown, while equity fund flows haven’t been universally negative since 2007 (2013-2015 saw notable inflows), the general trend has been the same for the past decade and counting: redemptions from equity funds, buying of bond funds.

Alphabet (GOOGL) Technical Issues

Below is a snapshot of GOOGL’s price chart from our Security Analysis page. Right before reporting earnings on Monday after the close, GOOGL made a fresh all-time high by barely eclipsing levels seen in mid-2018. The stock cratered after hours on Monday and opened sharply lower on Tuesday morning. This gap lower left shares below the steep uptrend channel that formed off the stock’s late 2018 low. Now the stock is in somewhat of a no-man’s land, and we’d expect meandering performance in the coming weeks as it tries to regain its footing. Start a two-week free trial to Bespoke Institutional to access our Security Analysis page and everything else we offer.

China ASHR ETF Dips Below 50-DMA

Chinese equity markets have been closed since Tuesday, but the ASHR ETF that tracks onshore China and trades on US exchanges has been trading, and yesterday it closed just below its 50-day moving average. This break below the 50-DMA is seen as a negative technical formation, but we’ll be watching it closely today to see how it closes out the week. Note that our trend algo still tags ASHR as being in an uptrend, and the sell-off over the last two weeks now leaves it with a “good” timing score. Start a two-week free trial to Bespoke Institutional to access our Security Analysis page and everything else we offer.